![]()

Products

We are actively taking measures to improve product quality levels.

Applications

Why Hamamatsu?

Support

Our company

Investors

Japan (EN)

Select your region or country.

Disclosure based on TCFD Recommendations

In August 2020, we announced our support for the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and promoted an analysis of the risks, opportunities, and financial impacts of climate change on our business. We are pleased to disclose some of the results of this study based on the TCFD recommendations.

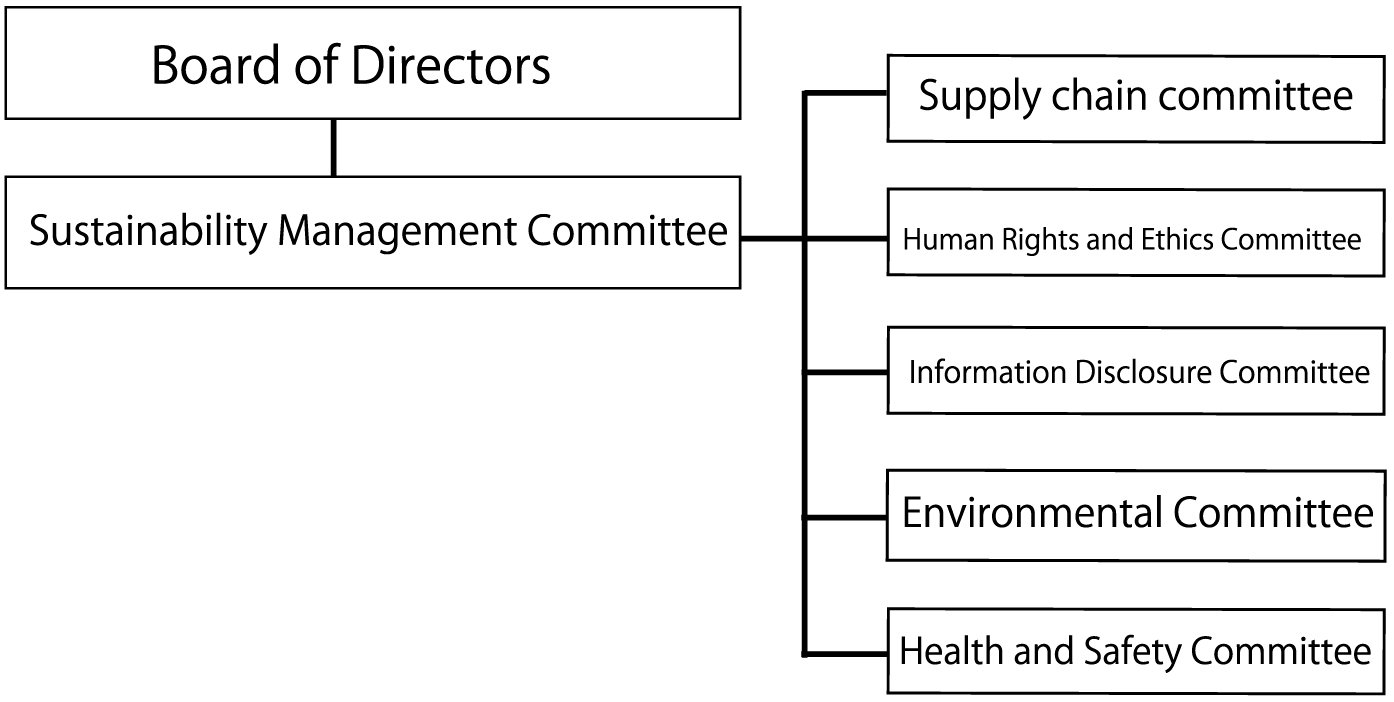

Governance

Based on our basic policy of sustainability and fundamental environmental policy, we recognize that initiatives for climate change is one of the most important issues. The contents of the studies conducted by the Environmental Committee and the Information Disclosure Committee, which are chaired by executive officers, as well as by its subcommittees and working groups under their supervision, are scrutinized by the Sustainability Management Committee, which is chaired by the officer in charge. The Sustainability Management Committee notifies Board of directors of the key issues. The PDCA cycle has implemented to ensure matters pointed out by Board of directors throughout the company.

<Detailed Information>

Basic policy of sustainability:

https://www.hamamatsu.com/jp/ja/our-company/sustainability/hamamatsu-photonics-sustainability.html

Hamamatsu Photonics Group Environmental Policy:

https://www.hamamatsu.com/jp/ja/our-company/sustainability/environment/environmental-management.html

Strategy

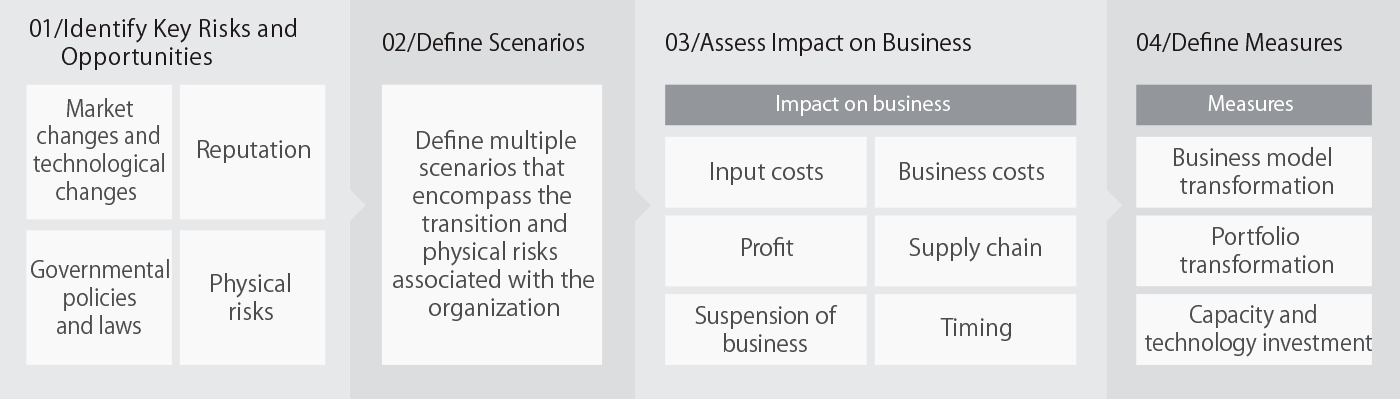

We recognize that various changes due to climate change will affect our business. In order to identify the most important risks and opportunities, we conducted a scenario analysis at 1.5/2°C and 4°C for our entire business in the following steps.

01 Identification of key risks and opportunities

We identified the climate change risks and opportunities facing the company now and in the foreseeable future. We scrutinized the interests of our stakeholders and their future significance. As a result, we identified 16 transition and physical risks and opportunities.

| Degree of Impact | Risks | Opportunities | |

|---|---|---|---|

| Transition | Physical | ||

| High | #1 Increase in operational costs due to introduction of carbon tax/emissions trading scheme #2 Increased burden and risk of fines due to stricter disclosure requirements and regulations #3 Loss of reputation among customers, decrease in sales, and loss of competitiveness #4 Short-term increase in operating costs due to introduction of renewable energy and promotion of energy conservation #5 Tighter regulations on raw materials |

#6 Increased risk of business shutdown and decreased sales due to severe wind and flood damage #7 Increased damage due to severe wind and flood damage #8 Increased air conditioning and cooling costs due to higher average temperatures #9 Increased risk of business shutdowns and decreased sales due to employees' inability to come to work due to higher average temperatures #10 Increased risk of business shutdown anddecreased sales due to employees' inability to come to work due to severe wind and flood damage |

#11 Increase in sales through the provision of products and services that contribute to addressing climate change #12 Increase revenues by entering new markets #13 Decrease in expenses due to gains in client and investor reputation #14 Increase in revenues through introduction of renewable energy and promotion of energy conservation |

Mild - Low |

#16 Loss of reputation and competitiveness among investors | ・Decrease in sales resulting from lower production due to lower rainfall at the water sources from which the water is withdrawn | |

02 Definition of scenario groups

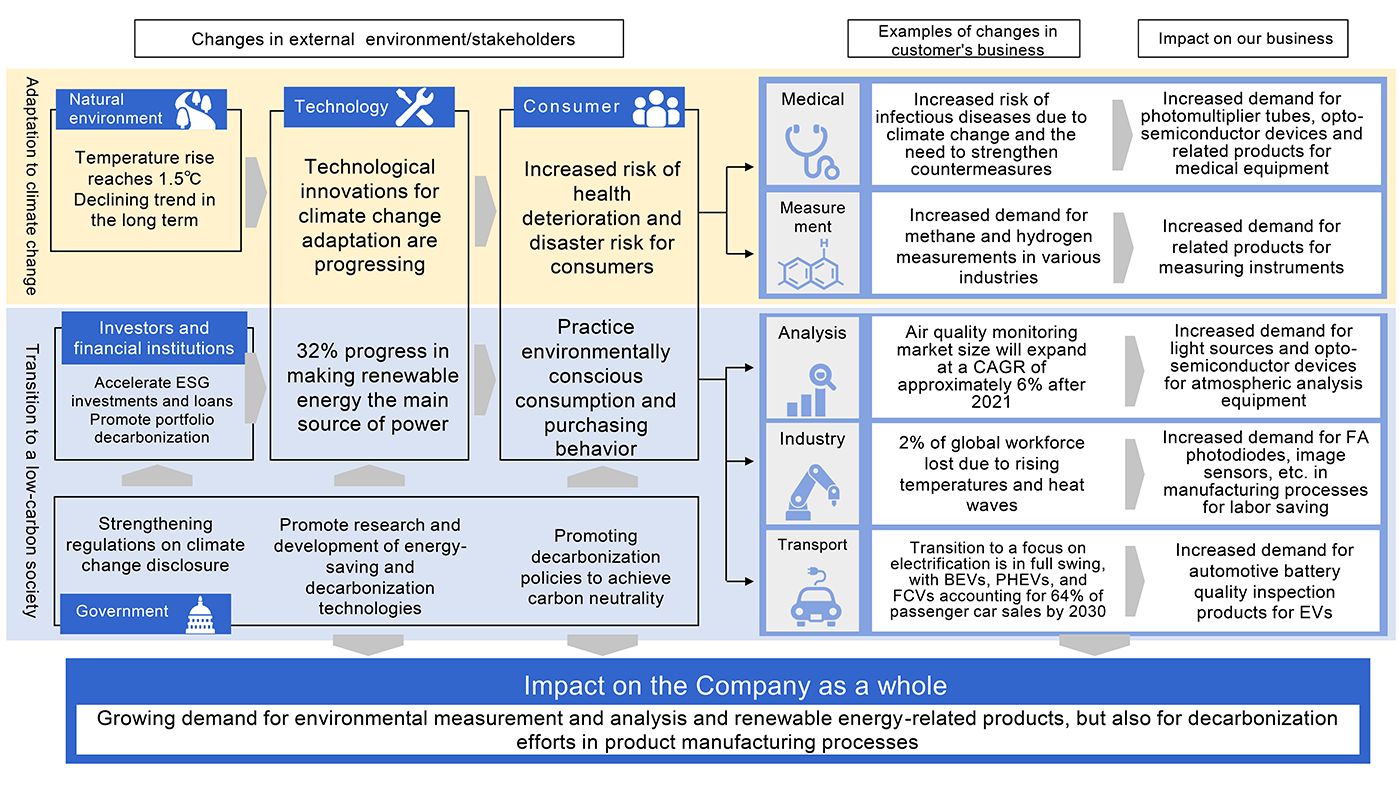

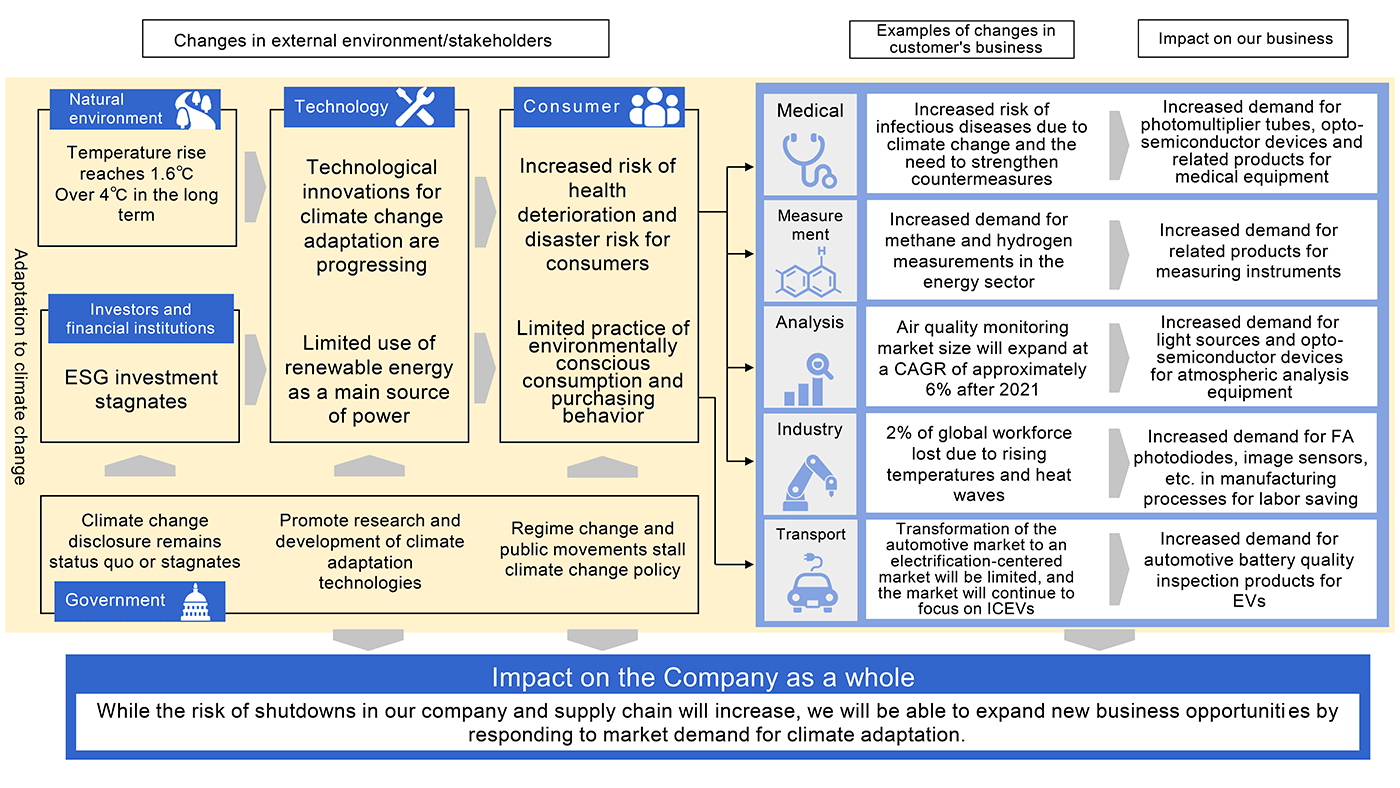

We set 1.5/2°C and 4°C scenarios for 2030 and considered changes in the external environment and stakeholders with regard to adaptation to climate change and the transition to a low-carbon society. We also projected changes in our customer sectors that may occur as a result of these changes, and examined the degree of impact on our business.

・Case of 1.5/2°C in 2030

・Case of 4°C in 2030

03 Business Impact Assessment

A sensitivity analysis was performed to assess the potential impact of each scenario on our strategic and financial position. For each of the climate change risks and opportunities with a high degree of importance, we examined the business impact calculation methods and calculated and examined them from available internal and external parameters. Examples are as follows;

| Types | Impact on Business in 2030 | Potential Financial Impact | ||

|---|---|---|---|---|

| 1.5/2℃ | 4℃ | |||

| Risks | Transitional | Decrease in sales due to lower product competitiveness and sluggish customer evaluations | High | - |

| Short-term increase in operating costs due to introduction of renewable energy and promotion of energy conservation | Mild | - | ||

| Physical | Business shutdowns (production sites, logistics, inventory, supply chain) and sales decline due to severe wind and flood damage | Mild | High | |

| Damage to manufacturing sites due to severe wind and flood damage and increased restoration costs | Mild | High | ||

| Opportunities | Medical and biotechnology equipment: Increased sales of related products for specimen testing equipment | Mild | Mild | |

| Industrial Equipment: Increased sales of related products for EV battery inspection systems | Mild | Mild | ||

| Analytical instruments: Increased sales of related products for environmental analysis | Mild | Low | ||

04 Consideration of countermeasures

Based on the results of the project impact assessment, we will consider countermeasures for those items that have a large impact.

Risk management

We have established environmental management rules and operate a company-wide environmental management system. We evaluate risks and opportunities for the environment, including climate change, and set environmental objectives and targets for each fiscal year. Management reviews our performance and challenges, and we strive to improve our environmental performance through continuous improvement.

Based on multiple climate-related scenarios, we have quantitatively evaluated risks and opportunities for financial impact, which will be used for risk management throughout the group in the future.

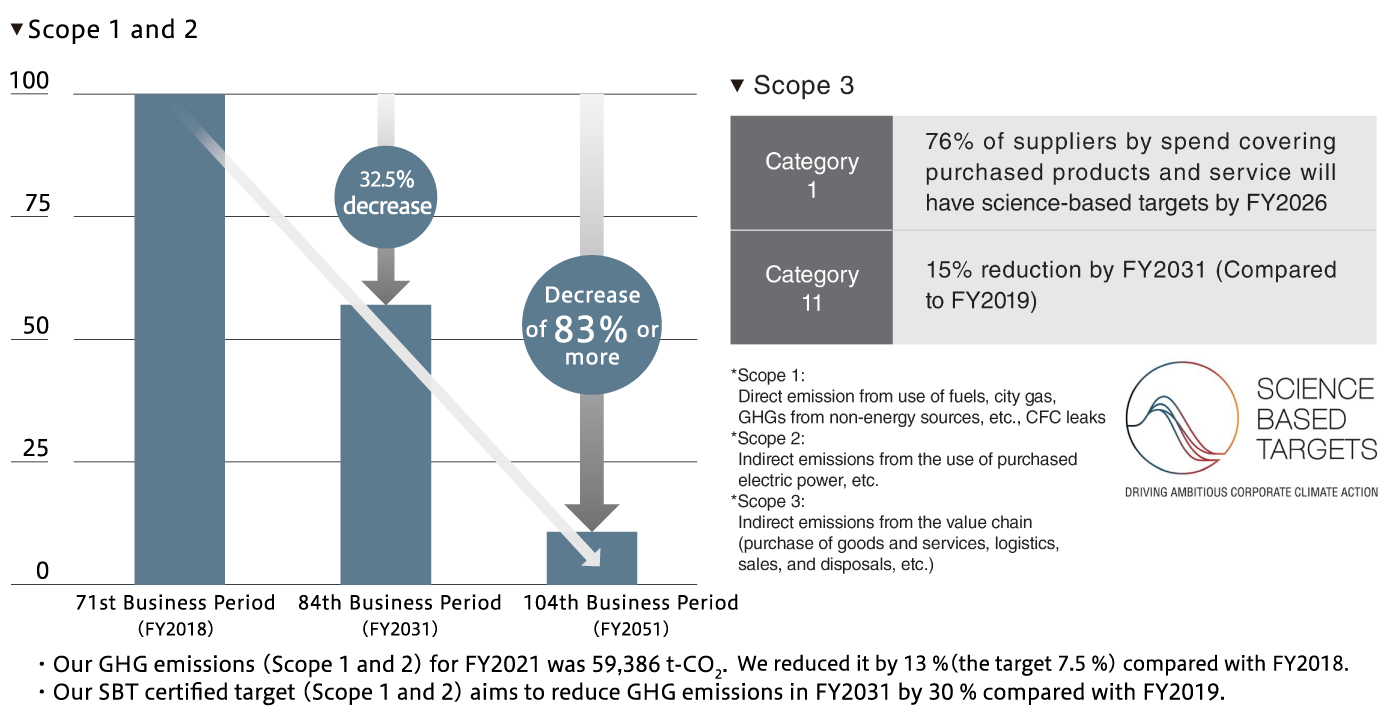

Metrics and Targets

Under the Group's long-term vision for global warming countermeasures, our greenhouse gas reduction targets (GHG reduction targets) were certified by the SBT Initiative, an international environmental organization, in October 2021 as scientifically based and in line with the Paris Agreement. Meanwhile, as key metrics in our mid- to long-term environmental strategy, we have established, evaluated, and managed GHG emissions, water usage, renewable energy usage, etc. GHG emissions are calculated for Scope 1, 2, and 3* in accordance with the GHG Protocol, and third-party verification is conducted. 74th fiscal year (ending September 30, 2021) GHG emissions (Scope 1 and 2) were 59,386 t-CO2 in the 74th fiscal year (ended September 30, 2021), a reduction of approximately 13 % (target 7.5 %) from the 71st fiscal year (ended September 30, 2018).

<Detailed Information>

Environment: https://www.hamamatsu.com/jp/jen/our-company/sustainability-and-csr/environment.html

ESG Data: https://www.hamamatsu.com/jp/en/our-company/sustainability-and-csr/esgdata.html

- Confirmation

-

It looks like you're in the . If this is not your location, please select the correct region or country below.

You're headed to Hamamatsu Photonics website for JP (English). If you want to view an other country's site, the optimized information will be provided by selecting options below.

In order to use this website comfortably, we use cookies. For cookie details please see our cookie policy.

- Cookie Policy

-

This website or its third-party tools use cookies, which are necessary to its functioning and required to achieve the purposes illustrated in this cookie policy. By closing the cookie warning banner, scrolling the page, clicking a link or continuing to browse otherwise, you agree to the use of cookies.

Hamamatsu uses cookies in order to enhance your experience on our website and ensure that our website functions.

You can visit this page at any time to learn more about cookies, get the most up to date information on how we use cookies and manage your cookie settings. We will not use cookies for any purpose other than the ones stated, but please note that we reserve the right to update our cookies.

1. What are cookies?

For modern websites to work according to visitor’s expectations, they need to collect certain basic information about visitors. To do this, a site will create small text files which are placed on visitor’s devices (computer or mobile) - these files are known as cookies when you access a website. Cookies are used in order to make websites function and work efficiently. Cookies are uniquely assigned to each visitor and can only be read by a web server in the domain that issued the cookie to the visitor. Cookies cannot be used to run programs or deliver viruses to a visitor’s device.

Cookies do various jobs which make the visitor’s experience of the internet much smoother and more interactive. For instance, cookies are used to remember the visitor’s preferences on sites they visit often, to remember language preference and to help navigate between pages more efficiently. Much, though not all, of the data collected is anonymous, though some of it is designed to detect browsing patterns and approximate geographical location to improve the visitor experience.

Certain type of cookies may require the data subject’s consent before storing them on the computer.

2. What are the different types of cookies?

This website uses two types of cookies:

- First party cookies. For our website, the first party cookies are controlled and maintained by Hamamatsu. No other parties have access to these cookies.

- Third party cookies. These cookies are implemented by organizations outside Hamamatsu. We do not have access to the data in these cookies, but we use these cookies to improve the overall website experience.

3. How do we use cookies?

This website uses cookies for following purposes:

- Certain cookies are necessary for our website to function. These are strictly necessary cookies and are required to enable website access, support navigation or provide relevant content. These cookies direct you to the correct region or country, and support security and ecommerce. Strictly necessary cookies also enforce your privacy preferences. Without these strictly necessary cookies, much of our website will not function.

- Analytics cookies are used to track website usage. This data enables us to improve our website usability, performance and website administration. In our analytics cookies, we do not store any personal identifying information.

- Functionality cookies. These are used to recognize you when you return to our website. This enables us to personalize our content for you, greet you by name and remember your preferences (for example, your choice of language or region).

- These cookies record your visit to our website, the pages you have visited and the links you have followed. We will use this information to make our website and the advertising displayed on it more relevant to your interests. We may also share this information with third parties for this purpose.

Cookies help us help you. Through the use of cookies, we learn what is important to our visitors and we develop and enhance website content and functionality to support your experience. Much of our website can be accessed if cookies are disabled, however certain website functions may not work. And, we believe your current and future visits will be enhanced if cookies are enabled.

4. Which cookies do we use?

There are two ways to manage cookie preferences.

- You can set your cookie preferences on your device or in your browser.

- You can set your cookie preferences at the website level.

If you don’t want to receive cookies, you can modify your browser so that it notifies you when cookies are sent to it or you can refuse cookies altogether. You can also delete cookies that have already been set.

If you wish to restrict or block web browser cookies which are set on your device then you can do this through your browser settings; the Help function within your browser should tell you how. Alternatively, you may wish to visit www.aboutcookies.org, which contains comprehensive information on how to do this on a wide variety of desktop browsers.

5. What are Internet tags and how do we use them with cookies?

Occasionally, we may use internet tags (also known as action tags, single-pixel GIFs, clear GIFs, invisible GIFs and 1-by-1 GIFs) at this site and may deploy these tags/cookies through a third-party advertising partner or a web analytical service partner which may be located and store the respective information (including your IP-address) in a foreign country. These tags/cookies are placed on both online advertisements that bring users to this site and on different pages of this site. We use this technology to measure the visitors' responses to our sites and the effectiveness of our advertising campaigns (including how many times a page is opened and which information is consulted) as well as to evaluate your use of this website. The third-party partner or the web analytical service partner may be able to collect data about visitors to our and other sites because of these internet tags/cookies, may compose reports regarding the website’s activity for us and may provide further services which are related to the use of the website and the internet. They may provide such information to other parties if there is a legal requirement that they do so, or if they hire the other parties to process information on their behalf.

If you would like more information about web tags and cookies associated with on-line advertising or to opt-out of third-party collection of this information, please visit the Network Advertising Initiative website http://www.networkadvertising.org.

6. Analytics and Advertisement Cookies

We use third-party cookies (such as Google Analytics) to track visitors on our website, to get reports about how visitors use the website and to inform, optimize and serve ads based on someone's past visits to our website.

You may opt-out of Google Analytics cookies by the websites provided by Google:

https://tools.google.com/dlpage/gaoptout?hl=en

As provided in this Privacy Policy (Article 5), you can learn more about opt-out cookies by the website provided by Network Advertising Initiative:

http://www.networkadvertising.org

We inform you that in such case you will not be able to wholly use all functions of our website.

Close